A look into Britain's macroeconomy

Or, how to navigate ourselves through tradeoffs

The most recent inflation figures revealed that the price of the average person's goods and services rose by 4.8% between December 2020 and December 2021. This is alarming, because it indicates that it is becoming more expensive for people to live, thus lessening their standard of living. Of course, this is mitigated by the fact that average pay has grown by 4.2% during the same period, however these gains have not been shared evenly and it is inevitable that many people will be considerably worse off because of the inflation.

Moreover, inflation often encourages more speculative investment to mitigate the erosion of savings’ real value often spurring more inflation. The economist Ricardo Reis has compared this to sitting on a beach trying to figure out, before it is too late, if a boat is drifting away from shore. Often once we realise inflation is causing us problems, it is simply too late to fix it.

Typically there are two main ways a central bank can deal with inflation: increase the bank rate, which will push up the cost of lending and thus discourage spending, or they may reduce the size of their balance sheet by selling bonds on the market, reducing the supply of money and thus pushing down inflation. However, both of these come with considerable drawbacks in that slowing down an economy will normally reduce growth and increase unemployment. Given growth has been considerably low since the Great Recession this also represents an un-ideal situation.

As is normal in economics this represents a trade-off. Either the Bank of England acts to clamp down on inflation and causes unemployment, or the Bank of England ignores the problem and it potentially grows worse.

Neither option seems ideal, so we have to assess what causes less harm. To do this it is important to understand the drivers of inflation because this will tell us a lot about how lasting it is, and also the likelihood of it growing worse. The reason this method is effective is broadly you can differentiate between two different types of inflation: transitory and permanent. Whilst both present harm, it is important to note that the former is much less worrisome than the latter. This is because it reflects a mere temporary increase in prices that will naturally disappear thanks to market forces causing supply to increase or demand to fall for a scarce good.

The classic example is that of an event that upsets the supply of oil. During the Arab Spring, the supply of oil produced in Libya fell by 1.6 million gallons per day. This made the supply of oil more scarce during a time of rising demand, thus increasing the price consumers must pay for the product. Given the impacts of oil prices on the wider economy this pushed overall inflation up. However, other countries were empowered to respond to this increase by increasing their own supply meaning in the long-run inflation was not affected and the risks to the wider economy were not substantial. We can see similar effects occurring for a wide range of commodity prices when supply shocks occur.

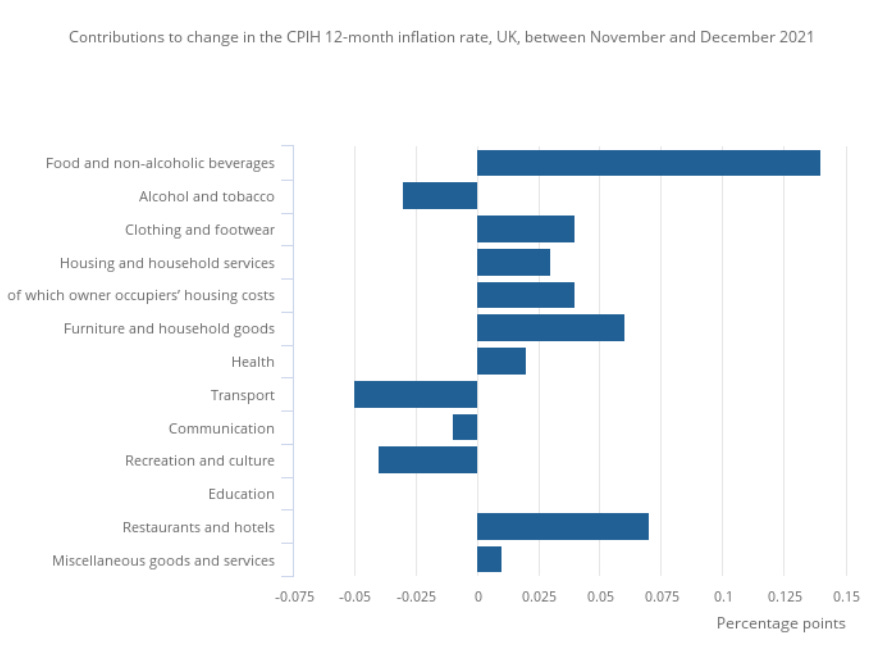

The data above breaks down the drivers of our current inflation and shows that a considerable amount of inflation comes from food, housing and household goods, restaurants and hotels, as well as clothing and footwear. Briefly, I’ll break down why I think we’re seeing rising prices in a few of these sectors.

Firstly, it is clear that food is the largest increase in that graph. This is particularly worrying given it is an essential item, and thus its impact will likely hit the poorest the most. Indeed, the IFS recently found that food and drink makeup over 20% of the bottom deciles expenditure compared to around 11% for the highest decile. According to a BBC article from November these increases are largely driven by pandemic related problems, such as labour shortages (worsened by post-Brexit immigration restrictions) and supply chain disruptions. It seems that we can blame Covid-19 for the bulk of these problems, therefore it seems unlikely that their effect will be lasting. This is consistent by the fact that food price rises can be observed throughout the developed world.

Housing and household costs also seems to be a major driver of our current inflationary episode. Indeed, this area has risen by its most amount since 2009 according to the ONS. This is largely driven by gas, which had already increased by 28.1% by November, and likely will be even larger now. There are multiple reasons for this occurring according to Simone Tagliapietra, a senior fellow at Bruegel. Demand has soared since production has returned now Covid restrictions aren’t in place, this winter has been colder than usual, coal is being phased out at an increasing rate, and a decline in wind production. On the other side, supply is struggling to keep up with this increased demand due to under-investment throughout the pandemic, and also due to a European wide phasing out of gas. Indeed, working gas in storage (blue line) can be seen decreasing throughout Europe, whereas demand is pretty constant (black line).

As explained above, the greater perceived profit that arise from these rising prices will incentivise an increase in supply mitigating these price increases in the long-run lowering their prices. This too is likely to be transitory.

It would be naive to suggest that all of this inflation will merely go away. As I explained in the beginning inflation, regardless of what caused it, is inflationary and we should continue to be cautious. Moreover, the Bank of England is tasked with ensuring price stability and if this gets out of hand it would ultimately undermine their long term ability to shape markets since investors will cease to trust their judgement.

For this reason, it seems the only sensible solution is to incrementally tighten monetary policy whilst avoiding any reactionary increases. The evidence seems to suggest that the inflation, all else held equal, will begin to decrease without Bank involvement. This is consistent with the Bank’s projection that inflation will continue to grow and peak at around 5% in April. However, it is essential that we do not underestimate the reactions of individuals and firms to avoid the erosion of savings that comes with inflation. Therefore, inaction does risk passively watching the boat drift out of shore and only reacting when it is too late to do so. This is why it seems to make sense that the Bank slowly taper expectations, and make it clear that they are prepared to act if inflation does get out of control.

Broadly, this seems to be exactly what they’re doing. To their credit, Andrew Bailey’s bank have resisted strong urges to increase rates, as MPC members Andy Haldane and Huw Pill have suggested, and ensure that the economy can recover uninterrupted. This has allowed GDP to return quickly to almost where it was before the pandemic.

According to the Bank of England, if they follow their market implied path then,

“GDP grows strongly in the near term as the recovery from Covid continues, but the pace of GDP growth slows thereafter. A degree of spare capacity is expected to emerge by the end of the forecast period. Inflation is a little above the MPC’s 2% target in two years’ time and just below it in three years.”

This would fit their mandate perfectly, and should only be considered a great success. To conclude this examination into the macroeconomy - the Bank of England should basically just keep doing what they’re doing. They couldn’t be doing better!